This article throws light upon the top nine methods for determining budget appropriation. The methods are: 1. The Percentage of Sales Method 2. Unit of Sales Method 3. Competitive Parity Method 4. Objective Task Method 5. Arbitrary Allocation Method 6. The Affordable Method 7. Sales Response & Decay Model 8. Communication Stage Model 9. Pay Out Planning Method.

1. The Percentage of Sales Method:

This method is most widely used method of setting the appropriation. In the past, the method enjoyed wide spread use. Today, although many firms use a combination of methods, they frequently report their advertising expenditures as a percentage of sales. Percentage of sales method is based on the previous year’s sales, on estimated sales of coming year or on some combination of these two.

In practice, when this method based on estimated future sales, may often actually work quite well. If virtually all conditions in the firm’s market including the general economic conditions and the competitive activity, remain rather constant, then it is quite possible that the same correlations will remain between the advertising and other sales and promotional activity expenditures and the resulting sales volume.

Using future sales does over come to a large extent the argument most frequently advanced against the use of percentage of past sales, which is that such a method ignores the fact that advertising should precede and is an important factor in stimulating demand and obtaining sales and is not something that follows sales. In other words, advertising should be considered the “cause” and not the “effect” of sales.

Merits:

1.There is a consistency between this approach and the standard accounting practice of handling advertising as one of the “operating expenses” that are usually analyzed in terms of there ratio to total sales volume. When the total marketing budget is determined in the overall marketing plan this method assigns a fixed proportion of that budget to advertising.

2. Percentage of sales is simple to calculate, and it is almost second nature for management to think of costs in percentage terms. Moreover, when it is wide spread throughout the industry, it results in advertising becoming proportional to market shares, and competitive war fare is made less probable.

3. They are related to increasing revenue and, thus, suggest that money will be available for advertising expenditures.

Demerits:

1. This method also presents a static approach to advertising rather than one that responds to the particular needs of market conditions. With a fixed multiplier, advertising expenditure increases as sales increases, and the tendency is to spend the exact ear marked amount, which may or may not be profitable.

3. As sales decline the expenditures of advertising decline, despite the possibility that it is at this point the demand may require that extra effort toward stimulation.

4. The percentage of sales method is not consistent with the basic marketing principle that advertising is an important factor in stimulating demand, and, as such precedes sales rather than being determined by sales.

2. Unit of Sales Method:

A variation of the percentage of sales method is the “fixed-sum-per-unit” appropriation technique. This method is also based on the premise that a specific amount of advertising is related to the marketing cost each unit produced rather than total sales volume.

It does not reflect price changes as does the percentage-of-sales method and it assumes that the amount of advertising effort needed to move a unit of merchandise is not closely related to increase or decrease in price. The advantage is that the manufacturer will know in advance how much the advertising cost of each unit of the product will be, which is especially useful in price determination.

3. Competitive Parity Method:

In this method, a manager establish budget amount by matching the percentage sales expenditure of the competitors. In essence, this method consists of setting the appropriation by relating it in some manner to the expenditures of the firm’s major competitor or competitors.

It leads to stability at the market place by minimizing marketing warfare. If companies know that competitors are unlikely to match their increases in promotional spending, they are less likely to take an aggressive posture to attempt to gain market share. This minimizes unusual or unrealistic advertising expenditure.

The demerits of this method includes:

1. It is a defensive strategy.

2. It is difficult to determine the competitor’s budget.

3. It assumes that because firms have similar expenditures, their programmes will be equally effective. This assumption ignores the contributions of creative executions and/or media allocations, as well as the success or failure of various promotions.

4. It ignores the fact that advertising and promotions are designed to accomplish specific objectives by addressing certain problems and opportunities.

5. There is no guarantee that the competitor will not increase or decrease its own expenditure, regardless of what other companies do.

6. Coke versus Pepsi and P & G VS HLL versus miller have been notorious for their spending wars, each responding to the others increased out lays.

7. It ignores possible advantages of the firm itself; some firms simply make better products than others.

8. There is no guarantee the competitor will continue to pursue their existing strategies. Since competitive parity figures are determined by examination of competitor’s previous years’ promotional expenditures, changes in market emphasis and/or spending may not be recognised until the competitor will not increase or decrease its own expenditures, regardless of what other companies do.

4. Objective Task Method:

Most often the funds for promotional efforts are decided upon before the detailed plans on how these funds are to be spent are worked out. But in this approach such plans are worked out before funds are allocated. In this method objective setting and budgeting go hand in hand rather than sequentially.

It is difficult to establish a budget without specific objectives in mind and setting objectives without regard to how much money is available make no sense. Objective task method is a build-up approach. Here, the funds are allocated to different advertising functions and media.

The objective task method of budget setting consists of following steps:

Step-I:

Defining the communication objectives to be accomplished.

Step-II:

Determining the specific strategies and task needed to attain these objectives.

Step-III:

Estimating the costs associated with performance of these strategies and tasks.

Step-IV:

Monitoring and evaluating the performance in the light of budget appropriated.

Step-V:

Reevaluating objectives.

When the objective task method is used, the first step is to set the objectives of the programme for the coming year or budget period. There may be one or several objectives, such as obtaining a certain volume of sales, obtaining a larger share of the market, entering a new area, or launching a new product.

Next, on the basis of experience or research findings, it is determined just what specific means will be necessary to achieve these objectives—the task involved.

Then it is necessary to determine how much and what kind of advertising will be required to accomplish the tasks established in the first two steps. At this point it may be advisable to take another step. The proposed appropriation for advertising is considered in light of the overall budget and financial position of the company.

If the amount involved appears to be excessive in view of the firm’s financial position and overall budget situation, it may be necessary to reconsider both the objectives and the proposed advertising plans and to modify them so that they will fit into the overall situation of the company.

In theory the objective task method would appear to be the best method of setting the advertising appropriation. It does not rely on any fixed relationship between advertising and sales. It is not bound by historical precedent.

In deciding how much and what kind of advertising will be necessary to achieve the objectives, full consideration can be given to the ever changing conditions in the market. It definitely relates the amount of money to be spend to the specific tasks required to achieve the established objectives.

The major problem with this method is the difficulty of determining which tasks will be required and the cost associated with each task.

With the present available methods of measuring the effectiveness of advertising, it is difficult to say with any real certainty just how much and what kind of advertising is required to achieve a certain result. Although the experienced advertiser uses the research methods available to answer such questions.

The objective task method offers advantages over other budgeting methods, but it has more difficulty in implementing when there is no track record for the product. So this method cannot be applicable for deciding advertising budget for the product which is in the introductory stage of the Product life cycle.

5. Arbitrary Allocation Method:

In this method, the budget is determined by the manager solely on the basis of his judgment, intuition or without any rule or rationality. In this method there is no systematic thinking, no objective setting and there is a complete ignorance of the advertising purpose.

6. The Affordable Method:

Also called as all you can afford method and the budget is based upon what the company can afford and is generally related to company’s profits or company assets. The approach is common among small firms.

7. Sales Response & Decay Model:

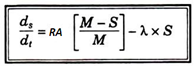

The method is proposed by vidale and wolfe. The model is based on the assumption that the shape of advertising (sales response function is known and the objective is to determine such a point that would optimize the advertising out lay/sales response ratio. The model measures the incremental changes in revenues at a given time relative to changes in the advertising budget at a time under a given set of situations.

The change in the rate of the sales at time is function of following factors:

(a) The sales response constant (Sales generated per advertising rupee)

(b) Sales decay constant (fraction of sales lost per time unit)

(c) The advertising budget.

(d) Saturation level of sales.

Mathematical relationship is

where,

Ds/dt = change in the rate of sales at time t

R = sales response constant

A = rate of advertising expenditure at time t

M = saturation level of sales (calculated through a study of product life cycle)

S = rate of sales at time t

λ = sales decay constant

Illustration 1:

A company’s advertising expenditure averages Rs. 5,000/-per month, current sales are Rs. 2,90,000/- and the saturation sales level estimated at Rs. 4,20,000/-, the sales response constant is Rs. 2/ – and the sales decay constant is 6% per month. Estimate the probable sales increase in next month.

Under the condition when the advertising expenditure is 5,000 per month, the sales would reduce by Rs. 14310/- i.e., it would reduce to 2,75,690. Hence the marketer is advised to increase the advertising budget to increase sales.

Illustration 2:

Ratio of sales advertising per rupee = 3 Current sales = Rs. 35,000/- Saturation level of sales = Rs. 1,50,000/- Company will loose 15% of sales per period if no advertising expenditure is made Advertising expenditure = Rs. 15,000/-

Thus, the sales generation would increase by Rs. 29,250 i.e., would reach to 64,250 if the advertising budget is 15,000 per month. This advertising budget would only be justified if the profit margin on this revenue is greater than Rs. 15,000/.

8. Communication Stage Model:

Designed by G. Ole, the model takes into consideration the impact of several variables that effect advertising expenditures to ultimate sales while formulating the size of the budget.

The procedure of budget setting involves the following steps:

Step-I:

Establishing the market share goal-Decide objectively as to what share of the market you can capture for example, we may went-10% of the market as our share.

Step-II:

Determining the percentage of market that we could reach by advertising for example, we may hope to reach 70% of the product users by our advertising campaign.

Step-III:

Determining the percentage of users of the product who are aware of our product and can be persuaded to try our brand.

Step-IV:

Determining the number of advertising exposures, considered for each percent of the market population for ex. 20 exposures are needed.

Step-V:

Determining the number of gross rating points (GPR) that would have to be purchased. Each GPR represent one exposure to 1% of population. For example, if each percent of target market require 20 exposures (GPR) and if we want to reach at 70% of the market, we would have to purchase 1400 GPRs.

Step-VI:

Total of budget = 1400 GPRs x Cost of each GPR Purchased.

9. Pay Out Planning Method:

This method is widely used for making advertising budget for the new product. A pay out plan is developed to determine how much to spend. The basic idea is to project the revenues the product will generate over two or three years, as well as the costs it will incur.

This method is based on the expected rate of return. This method will assist in determining how much advertising expenditures will be necessary when the return might be expected.

Though the payment plan is not always perfect, it guide the manager in establishing the budget. When used in conjunction with the objective and task method, it provides a much more logical approach to budget setting then the other budgeting approaches. In short, it can be said that there is no universally accepted method of setting a budget figure. Weaknesses in each method may make them unfeasible or inappropriate.

The use of the objective and tasks method continues to increase, where as less sophisticated methods are declining in favour. More advertisers are also employing the payout planning approach. By using these approaches in combination with the percentage of sales methods, these advertisers are likely to arrive at a more useful, accurate budget.

For example, may firms now start the budgeting process by establishing the objectives, the need to accomplish and then limit the budget by applying a percentage of sales or other methods to decide whether or not it is affordable. Competitor’s budgets may also influence this decisions.