Here is an essay on ‘Foreign Exchange Rate’ for class 11 and 12. Find paragraphs, long and short essays on ‘Foreign Exchange Rate’ especially written for school and college students.

Essay Contents:

- Essay on the Introduction to Foreign Exchange Rate

- Essay on the Foreign Exchange Quote

- Essay on the Types of Foreign Exchange Rates

- Essay on the Relationship between the Forward Rate and Spot Rate

- Essay on the Role of Triangular Arbitrage in Foreign Exchange Rate

- Essay on the Position of Currencies in Foreign Exchange

Essay # 1. Introduction to Foreign Exchange Rate:

The foreign exchange market is a 24-hour global market in which foreign currencies are bought and sold by central and commercial banks, businesses, investors, governments and speculators. The wholesale market (transactions between banks or inter-bank market) and a retail market (transactions between an authorized dealer and its clients) are the two components of a foreign exchange market. Regardless of location, every foreign exchange market adopts certain conventions with respect to exchange rate quotes and the manner in which deals are struck and settled.

ADVERTISEMENTS:

Differences exist in terms of scope; less developed exchange markets in some countries cannot offer the same communication and settlement facilities as that in say London or Tokyo can; nor can they offer foreign exchange quotes in numerous currencies. They also have fewer foreign exchange deals per day and lower trading volumes. The activities of foreign exchange department of a commercial bank revolve around foreign exchange quotes.

A bank’s foreign exchange activities are conducted by traders in the dealing room. Large international banks may have quantitative strategists, who give informed advice to traders in the dealing room, as well as to large corporate clients, upon request.

Traders conduct two types of trades:

1. Proprietary Trades:

ADVERTISEMENTS:

The AD’s foreign exchange traders buy or sell currencies and currency derivatives on behalf of the bank. For example, a bank expects that the rupee’s value will fall steeply against the US dollar over the next five business days, from its current rate of INR 40/USD. It buys 1 million USD for Rs. 40 million and holds for five business days. The bank sells the 1 million USD at the new exchange rate of INR 45.45/USD. Ignoring transaction costs, the bank makes a profit of Rs. 450,000 (45,450,000 – 40,000,000). In smaller banks, traders handle client trades and proprietary trades, but large banks have separate traders for proprietary trades.

2. Client-Driven Trades:

The AD’s foreign exchange traders buy or sell currencies and currency derivatives on behalf of their clients. For example, if a corporate client requires USD 1 million for delivery after 15 business days, the bank might buy the dollars ahead of the delivery date and hand over the amount to the client on the agreed date.

The AD’s dealing desk gives foreign exchange quotes in response either to a query from a client or from the desk of another authorized dealer. Every business day, the dealing desk in the foreign exchange department of an AD quotes its exchange rate for major currencies. Banks in India quote rates for 13 currencies. Their foreign exchange departments quote the exchange rate at the start of the day and this is communicated to all those branches that are authorized to conduct foreign exchange transactions. The first half an hour of each business day is the busiest time as queries about the exchange rate are dealt with at lightning speed.

ADVERTISEMENTS:

Essay # 2.

Foreign Exchange Quote:

ADVERTISEMENTS:

A foreign exchange quote is the exchange rate at which the AD is willing to deal in a particular currency pair. Each currency pair has its own foreign exchange quote. A currency pair may consist of the domestic currency and a foreign currency (rupee/ dollar, rupee/pound sterling, rupee/euro, and rupee/yen) or two foreign currencies (dollar/euro, or dollar/yen). The quote for a currency pair has a base currency, and a quote currency. A quote is read as ‘the base currency in terms of the quote currency’. In the quote Rs. 44.20/$, the base currency is the rupee, and the quote currency is the US dollar, and the quote is read as ‘Rs. 44.20 in terms of a dollar’.

i. Base currency – the currency quoted first

ii. Quote currency – the currency quoted second

ADVERTISEMENTS:

Currency Pairs:

Every currency pair has its own foreign exchange quote. For ‘n’ currencies, there are n (n – 1) currency pairs. There are 159 different currencies and hence there are 159 (159 – 1) = 25,122 currency pairs. But the most popular globally traded currency pairs are €/£, €/Yen, €/$, and $/£.

The International Organization for Standardization provides numerical and alphabetical codes (consisting of three of each) for each of the 159 currencies; code for the Indian rupee is INR and 356. However, many currencies are rarely traded or not traded at all. The most traded currency pairs are the euro/US dollar, US dollar/yen and US dollar /pound sterling. The euro/US dollar accounts for more than one-fourth of the turnover in the global foreign exchange market, followed by the US dollar/yen and the US dollar/pound sterling.

Essay # 3.

Types of Foreign Exchange Rates:

ADVERTISEMENTS:

Foreign exchange quotes may be denoted in different ways:

i. Direct Quote and Indirect Quote:

In a direct quote — or direct exchange rate — the domestic currency (H) is expressed in terms of 1 unit of a foreign currency (F). It is expressed as H/F. In an indirect quote — or indirect exchange rate — the foreign currency is expressed in terms of 1 unit of the domestic currency. It is expressed as F/H. If the AD giving the foreign exchange rate (whether direct or indirect) is willing to buy and sell the foreign currency, it is called a two-way quote. The buying rate is called the bid rate and the selling rate is called the ask rate. An AD who gives a two-way quote is called a market maker.

ii. Cross-Rate:

ADVERTISEMENTS:

If the exchange rate between a currency pair has to be calculated based on the exchange rates for two other currency pairs, then it is called a cross-rate. This happens because there is no quote for the given currency pair. Suppose a corporate client wants a foreign exchange quote on the Indian rupee and the Argentine peso. Every AD may be able to quote a rupee/US dollar rate and a peso/US dollar rate. But the rupee/peso rate may not be available since the peso is rarely traded in the Indian foreign exchange market. The client will have to calculate the cross-rate from the quotes for each of the other two currency pairs (rupee/US dollar rate and a peso/US dollar rate).

iii. Timing of Physical Delivery of Currencies:

If the physical delivery should happen within two business days of the day of entering into the contract, the quote is called the spot rate. If the physical delivery would happen at a pre-determined date in the future, it is called a forward rate.

iv. Counter-Party in the Quote:

ADVERTISEMENTS:

If an AD gets a query on the foreign exchange quote from another AD, then the latter quotes the inter-bank rate. If the AD gets a query on the foreign exchange quote from a client, it quotes the bill rate. When there is no lag in currency transfer, it is called a TT (telegraphic transfer) rate. They get their names from the method used to transmit currency from one location to another. If the AD converts one currency in a currency pair (either foreign exchange or domestic currency) into the other currency in the currency pair, and transfers it on the same day (by telex/fax/telegram) it is called a TT.

The exchange rate for a TT transfer is called the TT rate. If the bank buys a foreign Bill of Exchange, it will receive the funds only when it presents the bill on the due date. Thus, there is a delay in getting the foreign exchange. Therefore, the bank quotes the bill rate for such transactions.

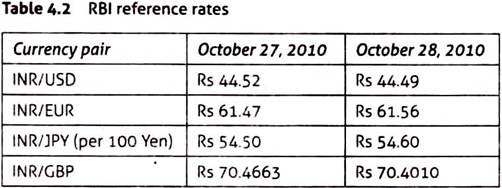

v. RBI Reference Rate:

A reference rate is based on the rates quoted by banks in Mumbai at 12 noon on each business day. The RBI uses these rates to calculate and provides reference rates for the rupee/pound sterling and the rupee/yen. They are direct rates available on RBI’s website. Except for the rupee/yen rate, the other three rates are per one unit of foreign currency—the rupee/euro reference rate on October 27, 2010 was Rs. 44.52 per euro. Table 4.2 gives the RBI reference rates on two different dates in October 2010.

Note that the reference rates are given up to the second decimal place, with the exception of the rupee/pound sterling, which is quoted up to the fourth decimal place. When the exchange rate is quoted up to the fourth decimal point, a pip refers to the fourth decimal place and the change is 1/100th of 1% (which is 0.0001).

ADVERTISEMENTS:

When the exchange rate is quoted up to the second decimal point, a pip refers to the second decimal place and the change is 1% (which is 0.01). Thus, an AD may start off with a quote of Rs. 43.55/USD at 10.30 am and as the day progresses, the exchange rate changes. By 11.30 am it may be quoting Rs. 43.56/USD, and by 12 noon it may be quoting Rs. 43.57/USD.

vi. Two-Way Quote:

In illustration 2, the US dollar was quoted against the peso, bolivar and pataca. For the AD in San Francisco, the direct quote states that $ 0.0179 = 1 MXN, $ 0.0125 = 1 VEB and $ 0.0667 = 1 MOP But they do not specify what the commercial bank intends to do. That is, would it buy or sell the dollar at the stated rate?

In practice, an AD quotes a foreign exchange rate for a particular currency pair in response to a query from another AD or a corporate client. The query does not specify whether the other party would buy or sell the foreign currency. Therefore, the trader gives both the quotes. A two-way quote specifies the exchange rate at which an AD would buy and sell the foreign currency in a currency pair.

Two-Way Quote in a Direct Exchange Rate:

A direct exchange rate or direct quote is one in which the domestic currency varies but the foreign currency against which it is quoted remains constant. Consider the following example of a two-way quote. It is also a direct quote because the domestic currency is quoted against a fixed amount of foreign currency.

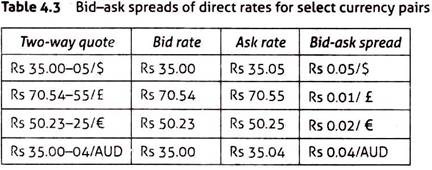

ADs give two-way quotes for several currency pairs. Every currency pair has its own bid rate, ask rate and bid-ask spread (Table 4.3). The ask rate is always greater than the bid rate in a direct exchange rate. The reason is easy to understand. Why does a market maker quote two rates for a currency pair? Because the difference between the bid and ask rates is his profit, or spread. If he is willing to give Rs. 33.77 in exchange for every CAD he buys, but expects to earn Rs. 33.79 for every CAD he sells, the bid-ask spread per CAD is Rs. 0.02 per CAD.

In a direct quote, will an AD give a two-way quote such that the bid rate is greater than the ask rate? The answer is no, because then, it stands to lose on its foreign exchange operations. In that case, obviously the higher the spread the greater is the gain per transaction for a market maker. Does this mean the AD can make two-way quotes such that the spread is as high as it wants? No again, because the foreign exchange market is fiercely competitive. Market makers must keep a careful eye on the two- way quotes offered by rivals in each currency pair, to ensure that it is not losing business in the quest for a larger margin. Table 4.4 shows the Rs/USD two-way quotes offered by two Indian banks at 10.30 am.

Note that both banks stand ready to sell the dollar at Rs. 45.15, that is, the ask rate for the US dollar is identical. However, for every dollar purchased, while Bank A is willing to pay only Rs. 45.13, Bank B will pay Rs. 45.14. Though Bank B will make less profit per transaction, those selling US dollars will prefer doing business with it. With the increasing integration of the Indian foreign exchange market, the size of the bid-ask spread in the spot market has decreased to levels as low as 25 paisa.

Two-way quote in an indirect exchange rate:

In an indirect quote, the domestic currency remains constant while the value of the foreign currency varies. The bid rate is always greater than the ask rate, with the difference being the AD’s spread.

ADVERTISEMENTS:

There is difference between the bid-ask the spread for the direct quote and the indirect quote. In the direct quote, the ask rate is larger than the bid rate, and the reverse is true in the indirect quote. The bid-ask spread for the direct quote is calculated as ask rate – bid rate, but in the indirect quote, it is calculated as bid rate – ask rate.

vii. Spot Rate:

It is the exchange rate agreed to on the contract date for the delivery of the two currencies within two business days. The day the deal is struck is called the ‘trade that the exchange of currencies takes place is called the ‘value date’ or ‘settlement date’. The spot rate is the exchange rate quoted for immediate exchange of each currency in the currency pair; here ‘immediate’ means within two business days. If the AD quotes a spot rate of Rs. 43.46-48/USD, it is a two-way quote. It means the AD stands ready to buy the US dollar for Rs. 43.46 and stands ready to sell the US dollar for Rs. 43.48.

The value date assumes importance in a spot rate because ‘immediate exchange’ of the currencies can mean any of the following:

i. The currency pair is exchanged on the day the deal is struck. If the deal for the exchange of the rupee for the US dollar is struck on April 21, the exchange of the currencies also takes place on April 21. The trade date and the value date are identical. This is called a ready transaction or a cash transaction.

ii. The currency pair is exchanged on the next business day after the trade date. This means if the deal for the exchange of the rupee for the US dollar is struck on April 21 (trade date), the exchange of the currencies takes place on April 22 (value date). The trade date and the value date are not identical—the value date is after the trade date. This is called a ‘Value TOM’ transaction, where TOM stands for tomorrow.

ADVERTISEMENTS:

iii. The currency is exchanged on the second business day after the trade date. This means if the deal for the exchange of the rupee for the US dollar is struck on April 21 (trade date), the exchange of the currencies takes place on April 23 (value date). The value date is the second business day after the trade date. This is called a spot transaction.

Where the value date and the trade date are not identical in a spot contract between two parties, the value date is always calculated using business days. That is, suppose in the above example April 22 was a Sunday, the value date in case (b) would be April 23, and the value date in case (c) would be April 24. In international foreign exchange markets, the value date in a spot transaction is two business days after the trade date.

It is the AD who makes the market (that is, gives a two-way quote in response to a query) that determines the value date. Suppose a European bank based in Brussels was the market maker in a spot transaction with an American corporate client, in a deal to exchange 1 million euros for US dollars. The trade date of the contract is Tuesday, and the value date is Thursday. If Thursday is a holiday in Europe, the European bank delivers the euros and collects the US dollars on Friday.

A market maker gives spot rates as two-way quotes (bid rate and ask rate). Recall that in a direct quote, the ask rate is greater than the bid rate, and in the indirect quote the bid rate is greater than the ask rate. Two-way quotes may be quoted only in decimals.

Suppose the spot rates at 10.30 am for the Rs/US$ in the past three days have been:

Rs. 43.44-45/US$

ADVERTISEMENTS:

Rs. 43.45-46/US$

Rs. 43.47- 48/US$

It may be noted that Rs. 43 is a constant in all the three quotes and only the decimals in the bid rate and ask rate changed from day to day. For instance on day 1, the bid rate and ask rate were Rs. 43.44 and Rs. 43.45 respectively, and on day 2 the bid and ask rates were Rs. 43.45 and Rs. 43.46 respectively. The AD may quote ’47-48′ on Day 3. From this it must be interpreted that the bid and ask rates are Rs. 43.47/$ and Rs. 43.48/$ respectively.

viii. Forward Rate:

It is the exchange rate agreed upon for the delivery of the two currencies beyond two business days from the trade date. Usually, forward rates are quoted for delivery after one month or two months. The month in which the delivery date of a forward transaction occurs is called the spot month.

Suppose a client approaches the AD on April 1 and wants to enter into a forward contract to sell $300,000 for rupees for delivery in one month. The AD quotes a rate of Rs. 42.50-55/USD. The details of the contract are- Trade date is April 1. Value date is calculated as one month after the spot date (i.e., April 3); therefore, the value date is May 3. If May 3 is a holiday, then the value date is May 4. Forward rate is Rs. 42.50/USD (bid rate, since from the AD’s point of view, it will be buying the dollars).

On May 3, the client will hand over $300,000 to the AD and receive (Rs. 42.50) ($300,000) = Rs. 12,750,000 from the AD (ignoring transaction costs).

Why would the client want to enter into a forward contract to sell $300,000 for rupees at the pre-determined exchange rate of Rs. 42.50/US$? Perhaps he is not sure of what the Rs/$ spot rate will be on May 3.

Calculation of Forward Rate:

The forward rate is calculated with reference to the spot rate. Upon receiving a query for a 1-month forward rate for a currency pair, an AD gives the forward margin (also known as swap points), that corresponds to the spot bid rate and the spot ask rate respectively.

This is used to determine the forward rate in the manner described below:

Direct Quote (H/F):

a. When the swap points are in ascending order:

i. The swap points represent a forward premium.

ii. The swap points should be added to the spot bid rate and the spot ask rate respectively

iii. Therefore, forward bid rate > spot bid rate

forward ask rate > spot ask rate

b. When the swap points are in descending order:

i. The swap points represent a forward discount.

ii. The swap points should be deducted from the spot bid rate and the spot ask rate respectively.

iii. Therefore, forward bid rate < spot bid rate

forward ask rate < spot ask rate

Indirect Quote (F/H):

a. When the swap points are in descending order:

i. The swap points represent a forward premium.

ii. The swap points should be deducted from the spot bid rate and the spot ask rate respectively.

iii. Therefore, forward bid rate < spot bid rate

forward ask rate < spot ask rate

b. When the swap points are in ascending order:

i. The swap points represent a forward discount

ii. The swap points should be added to the spot bid rate and the spot ask rate respectively

iii. Therefore, forward bid rate > spot bid rate

forward ask rate > spot ask rate

Annualized Forward Premium:

The annualized forward premium is the ‘n’ period forward premium calculated for the whole year and expressed as a percentage.

It is calculated as:

![]()

where,

F = forward rate

S = spot rate

F – S = forward premium

n = the period of the forward contract (in days)

What if there is a forward discount? Then, the same formula is applied with forward discount replacing forward premium.

ix. Inter-Bank Rate:

As the name indicates this is the spot rate or the forward rate quoted by one AD to another in the inter-bank market. The inter-bank rates are typically lower than merchant rates (which are spot rates or forward rates quoted by an AD to its clients). Thus, on a particular day, the SBI may quote a spot rate of Rs. 43.44-46/US$ in the inter-bank market and a 1-month forward rate of Rs. 43.47-49/US$.

If SBI wants to enter into a deal in the spot market or the forward market with its client, its spot and forward exchange rates (called merchant rates) will be higher than those quoted in the inter-bank foreign exchange market. This is to cover the bank’s costs. The exchange margin is the difference between the exchange rate quoted by a bank to its client and the inter-bank rate.

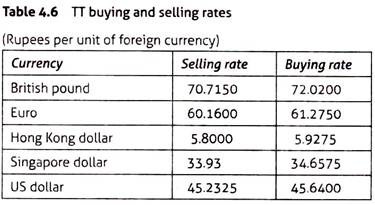

x. TT Rate:

TT refers to telegraphic transfer. Though ‘TT’ stands called telegraphic transfer, the TT rate applies to any transaction in foreign exchange where mail transfer or payment through demand draft occurs. Financial newspapers like the Economic Times, or the Business Standard, provide TT buying rate and TT selling rate for different foreign currencies. The TT rates for currencies as on September 24, 2010 are shown in Table 4.6. Each is a direct rate and refers to the number of rupees per unit of foreign currency. Note that the buying rate is lower than the selling rate. The TT rate is the inter-bank rate minus the exchange margin.

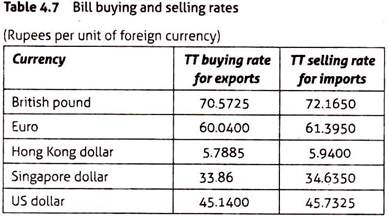

xi. Bill Rate:

Bills of Exchange are negotiable instruments. They are of two types—sight bills and usance bills. A sight bill can be presented by the holder after a certain number of days have elapsed. A usance bill can be presented by the holder only on the maturity date of the bill, and is payable on that date. It is a part of the documents in international trade. The bank checks the documentation in an international trade transaction with regard to its authenticity and adequacy.

Thus, they impose a margin. Bill rates play an important part of the documentation in import and export trade. Commercial banks are crucial intermediaries in international trade transactions. The rate at which a bank buys a bill is called the buying rate. The rate at which a bank sells a bill is called the selling rate. Table 4.7 shows the rates in export and import transactions.

Essay # 4.

Relationship between the Forward Rate and Spot Rate:

Normally an ‘n’ period forward rate, such as the 1-month forward rate is never equal to the current spot rate. The forward rate for the INR/USD has been either greater than or less than the spot rate, because the forward rate is influenced by a number of factors including market expectations, the demand and supply of the dollar, and interest rate differentials in India and USA.

When the domestic currency is freely convertible, expectations are affected by interest rates, but when there are restrictions on convertibility as in India, expectations are affected by anticipated future demand for and supply of a specific foreign currency in a currency pair.

Forward premia in India are ‘significantly influenced’ by ‘supply and demand of forward US dollars, interest differentials and expectations of future interest rates; and expectations of future US dollar-rupee exchange rate’. In the Indian foreign exchange market, demand and supply are the principal factors determining forward rates. Research shows that the forward rate overestimates the ‘n’ period spot rate in the Indian foreign exchange market, and is not an accurate predictor of future spot rate.

Essay # 5. Role of

Triangular Arbitrage in Foreign Exchange Rate:

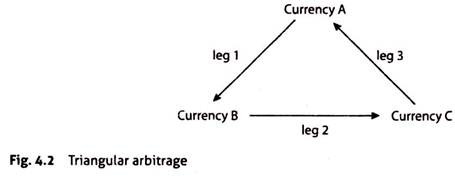

A cross-rate is the exchange rate between two currencies that are each expressed in terms of a third currency. The third currency is called the ‘vehicle’ currency. Suppose there are three currencies A, B and C. Currency B is expressed in terms of A and currency C is also expressed in terms of A. Therefore, currency A is the vehicle currency. But currencies B and C are not expressed in terms of each other. A cross-rate is the exchange rate between currency B and C using the exchange rates between currencies A and B, and currencies A and C.

That is:

![]()

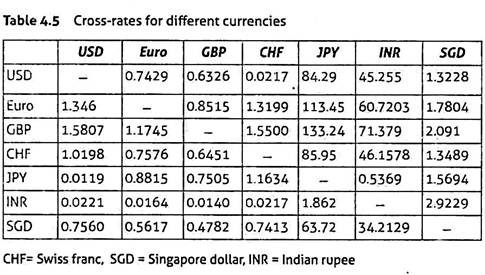

Table 4.5 shows the cross-rates for major currencies as on September 24, 2010. Each row gives the number of units of a currency with respect to one unit of a currency in the first column. For example, the INR/USD rate shows that Rs. 45.255 = 1USD. The USD/SGD rate is USD 0.7560/SGD.

Suppose, one wants the INR/SGD cross-rate, it is computed as follows:

INR/SGD = (USD/SGD) (INR/USD)

= ($ 0.7560/1) (Rs. 45.255/1) = Rs. 34.21278/SGD ≈ Rs. 34.2129

Compare this rate with that in the table. Both are identical.

When the cross-rate as calculated above is either greater or lower than it should be, there is a possibility for profit making without taking any risk. Triangular arbitrage is the process of making a profit by exploiting the discrepancy between the actual cross-rate and what the cross-rate ought to be. It gets its name from the manner in which a market participant moves from one currency to another and then to a third, so as to make a profit. Figure 4.2 depicts triangular arbitrage. In leg 1, currency A is sold in exchange for currency B. In leg 2, currency B is sold in exchange for currency C. In leg 3, currency C is sold in exchange for currency A.

How can an opportunity for triangular arbitrage be spotted? By comparing the quotes prevailing for three currency pairs, with what should actually prevail. Take the three currency pairs given in Fig. 4.2.

This can be expressed as:

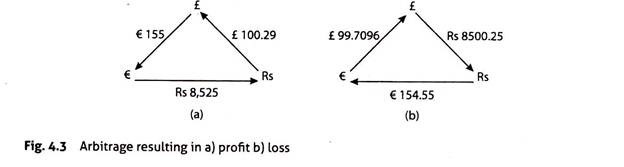

In other words, triangular parity should exist, no matter which currency pair you equate with the product of the two other currency pairs. If this condition is violated because the trading desks of different banks are quoting rates that do not result in triangular parity, then an alert participant will realize that opportunities for arbitrage exist and would choose to exploit them. Suppose, Citibank gives quote of Rs. 85.0025/£, while Barclays Bank gives a quote of Rs. 55/€. BNP Paribas gives a quote of € 1.55/£. Let us verify whether triangular parity exists.

The quotes available are INR 85.0025/£ Rs. 55/€ €1.55/£

Putting these values into equation 1: = (Rs. 55/€) (€1.55/£) = Rs. 85.25/£

But, INR 85.25 ≠ 85.0025 (the quoted INR/€ rate). Hence, arbitrage opportunities exist. Assume that the participant has £ 100 (this is just a notional figure, and any amount can be used). He decides to move from currency to currency, and concludes three deals within a few minutes. The deal (ignoring transaction costs) sees him moving from pound to euro to rupee.

1. He sells £100 and buys euros = (£100) (€1.55) = €155

2. He sells €155 and buys rupees = (€155) (55) = Rs. 8525

3. He sells Rs. 8,525 and buys pounds = Rs. 8,525 ÷ 85.0025 = £100.29

Thus, ignoring transaction costs, he began with £100 and ended a few minutes later with £100.29 (Fig. 4.3a). Typically, the discrepancies are very small and will be quickly exploited by market participants, such as trading desks of international banks. The above example is an extreme case. In reality, discrepancies exist only in the third or fourth decimal places of the currency pairs.

An alert observer who is tracking the exchange rates will be able to make a profit with just a couple of phone calls. The size of his profit depends on the initial position. Like, him, many others also make use of the discrepancy to make risk-less profit. Their arbitrage actions bring the rates into parity once again.

Suppose, however he moves between the three currencies in the other direction? That is, he moves from pounds to rupees to euros? This will not generate profits for him, as shown in Fig. 4.3b. Assuming he starts with an initial amount of £100, he ends up making £99.7096 at the end.

Triangular arbitrage yields profits only when the movement from currency to currency is in one direction. How can this direction be identified? The rule is to always buy an undervalued currency. How does one identify an undervalued currency? Take the above example, where a market participant has an initial long position of £100. He must sell the pound and buy either the rupee or the euro.

He compares the quoted INR/£ rate and the €/£ rate with their respective cross-rates:

i. The quoted rate for INR/£ is Rs. 85.0025/£ – The rupee is overvalued because the market participant needs fewer rupees (Rs. 85.0025) to buy a pound, than would be needed under the cross-rate (Rs. 85.25).

ii. The quoted rate for €/£ is €1.55/£ – The euro is undervalued because the market participant needs more euros (€1.55) to buy a pound, than would be needed under the cross-rate (€1.547).

So he moves from the pound to the euro, then to the rupee and back to the pound.

Essay # 6.

Position of Currencies in Foreign Exchange:

On every business day, ADs buy and sell different currencies. At the end of a business day, if the sales of a specific foreign currency are not equal to the AD’s purchases in the foreign currency, the bank is said to have an open position. Suppose the AD bought $100 million and sold $70 million during the business day. It has a net open position of $30 million. It is said to have gone ‘long’ on the dollar.

If the AD bought $100 million and sold $120 million, it is said to have gone ‘short’ on the dollar. This is also called an oversold position. If the AD bought $100 million and sold $100 million, it is said to have a ‘square’ position in US dollars. An AD with an overbought or oversold position in a specific foreign currency is exposed to position risk (or rate risk). Position risk is the risk of erosion of the bank’s foreign exchange asset holdings due to a change in the exchange rates. The position of a bank in a particular foreign currency is determined by aggregating the purchases and sales in that foreign currency by all its branches.

The RBI permits Indian banks to undertake intra-day trading in foreign exchange. The RBI monitors open positions, and stipulates the daily maximum of an open position in each foreign currency that a bank can have on any business day. The maintenance of a ‘square’ or ‘near square’ position has to be complied with by every bank at the close of each business day.

As a part of its risk management activities, each bank sets a ceiling on an open position in foreign currency, at the end of every business day. This is called an ‘overnight’ limit. Foreign exchange dealers in the dealing room keep this ceiling in view while transacting trades. Since foreign exchange is subject to wide fluctuations, banks prefer to cover their open positions in foreign exchange.