This article throws light upon the top two ways for financial evaluation of leasing. The ways are: 1. Lessee’s Point of View 2. Lessor’s Point of View.

Financial Evaluation of Leasing: Way # 1.

Lessee’s Point of View:

(Lease or Buy/Lease or Borrow Decisions):

Once a firm has evaluated the economic viability of an asset as an investment and accepted/selected the proposal, it has to consider alternate methods of financing the investment. However, in making an investment, the firm need not own the asset. It is basically interested in acquiring the use of the asset.

ADVERTISEMENTS:

Thus, the firm may consider leasing of the asset rather than buying it. In comparing leasing with buying, the cost of leasing the asset should be compared with the cost of financing the asset through normal sources of financing, i.e., debt and equity.

Since, payment of lease rentals is similar to payment of interest on borrowings and lease financing is equivalent to debt financing, financial analysts argue that the only appropriate comparison is to compare the cost of leasing with that of cost of borrowing. Hence, lease financing decisions relating to leasing or buying options primarily involve comparison between the cost of debt-financing and lease financing.

The evaluation of lease financing decisions from the point of view of the lessee involves the following steps:

(i) Calculate the present value of net-cash flow of the buying option, called NPV (B).

ADVERTISEMENTS:

(ii) Calculate the present value of net cash flow of the leasing option, called NPV (L)

(iii) Decide whether to buy or lease the asset or reject the proposal altogether by applying the following criterion:

(a) If NPV (B) is positive and greater than the NPV (L), purchase the asset.

(b) If NPV (L) is positive and greater than the NPV (B), lease the asset.

ADVERTISEMENTS:

(c) If NPV (B) as well as NPV (L) are both negative, reject the proposal altogether.

Since many financial analysts argue that the lease financing decisions arise only after the firm has made an accept-reject decision about the investment; it is only the comparison of cost of leasing and borrowing options.

The following steps are involved in such an analysis:

(i) Determine the present value of after-tax cash outflows under the leasing option.

ADVERTISEMENTS:

(ii) Determine the present value of after-tax cash outflows under the buying or borrowing option.

(iii) Compare the present value of cash outflows from leasing option with that of buying/borrowing option.

(iv) Select the option with lower presented value of after-tax cash outflows.

We have illustrated the above analysis in the following illustrations.

ADVERTISEMENTS:

Illustration 1:

A limited company is interested in acquiring the use of an asset costing Rs. 5,00,000. It has two options:

(i) To borrow the amount at 18% p.a. repayable in 5 equal installments or

(ii) To take on lease the asset for a period of 5 years at the year end rentals of Rs. 1,20,000.

ADVERTISEMENTS:

The corporate tax is 50% and the depreciation is allowed on w.d.v. at 20%. The asset will have a salvage of Rs. 1,80,000 at the end of the 5th year.

You are required to advise the company about lease or buy decision. Will decision change if the firm is allowed to claim investment allowance at 25%?

Note:

(1) The present value of Re. 1 at 18% discount factor is:

ADVERTISEMENTS:

1st year – .847

2nd year – .718

3rd year – .609

4th year – .516

5th year – .437

(2) The present value of an annuity of Re. 1 at 18% p.a. is Rs. 3.127.

ADVERTISEMENTS:

Solution:

(v) Evaluation:

As the present value of after-tax cash outflows under the leasing option is lesser than the present value of after-tax cash outflows of the buying option, it is advisable to take the asset on lease.

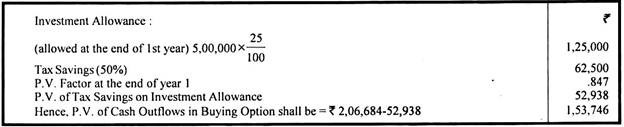

(vi) Decision if Investment Allowance is allowed:

ADVERTISEMENTS:

In case Investment Allowance is allowed on purchase of asset the total of present value of net cash outflows will decrease by the present value of tax savings on investment allowance as below:

In that case, the P.V. of cash outflows under buying option shall be lesser than the P.V. of cash outflows under leasing option and the company should buy the asset.

Financial Evaluation of Leasing: Way # 2.

Lessor’s Point of View:

The financial viability of leasing out an asset from the point of view of lessor can be evaluated with the help of the two time adjusted methods of capital budgeting:

(a) Present Value Method

ADVERTISEMENTS:

(b) Internal Rate of Return Method.

(a) Present Value Method:

This method involves the following steps:

(i) Determine cash outflows by deducing tax advantage of owning an asset, such as investment allowance, if any.

(ii) Determine cash inflows after-tax as below:

(ii) Determine the present value of cash outflows and after tax cash inflows by discounting at weighted average cost of capital of the lessor.

ADVERTISEMENTS:

(iv) Decide in favour of leasing out an asset if P.V. of cash inflows exceeds the P.V. of cash outflows, i.e., if the NPV is +ve; otherwise in case N.P.V. is -ve, the lessor would lose on leasing out the asset.

The above technique has been explained with the help of the following example.

Illustration 2:

From the information given below, you are required to advise about leasing out of the asset:

Solution:

Since the present value of cash inflows is more than the present value of cash outflows or says N.P.V. is positive, it is desirable to lease out the asset.

(b) Internal Rate of Return Method:

The internal rate of return can be defined as that rate of discount at which the present value of cash- inflows is equal to the present value of cash outflows.

It can be determined with the help of the following mathematical formula:

C = A1/(1+r) + A2/(1+r)2 + A3/(1+r)3 + … … … … + An/(1+r)n

where, C = Initial Outlay at time Zero.

A1, A2, … … … An = Future net cash flows at different periods.

2,3 …….. , = Numbers of years

r = Rate of discount of internal rate of return.

The Internal rate of return can also be determined with the help of present value tables.

The following steps are required to practice the internal rate of return method:

(1) Determine the future net cash flows for the period of the lease. The net cash inflows are estimated future net cash flows for the period of the lease. The net cash inflows are estimated future earnings, from leasing out the asset, before depreciation but after taxes.

(2) Determine the rate of discount at which the present value of cash inflows is equal to the present value of cash outflows. This may be determined as follows:

(a) When the annual net cash flows are equal over the life of the asset:

Firstly, find out Present Value Factor by dividing initial outlay (cost of the investment) by annual cash flow, i.e., Present Value Factor = Initial Outlay/Annual Cash Flow. Then, consult present value annuity tables with the number of year equal to the life of the asset and find out the rate at which the calculated present value factor is equal to the present value given in the table.

Illustration 3:

Solution:

(b) When the annual cash flows are unequal over the life of the asset:

In case annual cash flows are unequal over the life of the asset, the internal rate of return cannot be determined according to the technique suggested above. In such cases, the internal rate of return is calculated by hit and trial and that is why this method is also known as hit and trial yield method.

We may start with any assumed discount rate and find out the total present value of all the cash flows by consulting present value tables.

The so calculated total present value of cash inflows as compared with the present value of cash outflows which is equal to the cost of the initial investment where total investment is to be made in the beginning. The rate, at which the total present value of all cash inflows equals the initial outlay, is the internal rate of return. Several discount rates may have to be tried until the appropriate rate is found. The calculation process may be summed up as follows.

(i) Prepare the cash flow table using an arbitrary assumed discount rate to discount the net cash flow to the present value.

(ii) Find out the Net Present Value by deducting from the present value of total cash flows calculated in (i) above the initial cost of the investment.

(iii) If the Net Present Value (NPV) is positive, apply higher rate of discount.

(iv) If the higher discount rate still gives a positive net present value, increase the discount rate further until the NPV becomes negative.

(v) If the NPV is negative at this higher rate, the internal rate of return must be between these two rates:

(3) Accept the proposal if the internal rate of return is higher than or equal to the minimum required rate of return, i.e. the cost of capital or cut off rate.

(4) In case of alternative proposals select the proposal with the highest rate of return as long as the rates are higher than the cost of capital or cut-off rate.

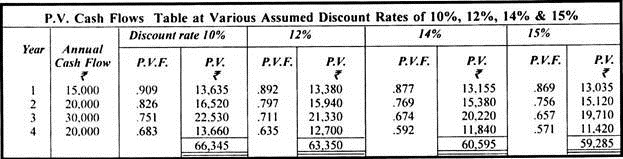

Illustration 4:

Initial Investment – Rs. 60,000

Life of the Asset – 4 years

Estimated Net Annual Cash Flows:

Compute the internal rate of return and also advise the lessor about the leasing out decision if his expected minimum rate of return is 15%.

Note:

Present Value Factor at various rates of discount.

(1) The present value of cash flows at 14% rate of discount is Rs. 60,595 and at 15% rate of discount it is t 59,285. So the initial cost of investment which is Rs. 60,000 falls in between these two discount rates. At 14% the NPV is+ 595 but at 15% the NPV is – 715, we may say that IRR = 14.5% (approx).

(2) As the IRR is less than the minimum required rate of return, the lessor should not lease out the asset.