After reading this article you will learn about the procedures for materials, purchase and stores management.

Materials Management:

Most manufacturing concerns spend more than 60% of the money they take in, for materials, i.e., materials soak up a substantial portion of the capital invested in an industrial concern. This emphasizes the need for adequate materials management and control because even a small saving in materials can reduce the production cost to a fair extent and thus add to the profits.

Materials Management may be thought of as an integrated functioning of the different sections of a company dealing with the supply of materials and other related activities so as to obtain maximum co-ordination and optimum minimum expenditure on materials. Materials Management involves controlling the type, amount, location, movement, timings of purchase of various materials etc., used in an industrial concern.

Functions of Materials Management:

(i) Materials planning.

(ii) Procurement or purchasing of materials.

(iii) Receiving and warehousing.

(iv) Storage and store-administration.

(v) Inventory control.

(vi) Standardization, Simplification and Value-analysis.

(vii) External transportation (i.e., traffic, shipping, etc.) and materials handling (i.e., internal transportation).

(viii) Disposal of scrap, surplus and obsolete materials.

Objectives of Materials Management:

(i) To minimize materials cost.

(ii) To procure and provide materials of desired quality when required, at the lowest possible overall cost of the concern.

(iii) To reduce investment tied in inventories for use in other productive purposes and to develop high inventory turnover ratios.

(iv) To purchase, receive, transport (i.e., handle) and store materials efficiently and to reduce the related costs.

(v) To trace new sources of supply and to develop cordial relations with them in order to ensure continuous material supply at reasonable rates.

(vi) To cut down costs through simplification, standardization, value analysis, import substitution, etc.

(vii) To report changes in market conditions and other factors affecting the concern, to the concern.

(viii) To modify paper work procedure in order to minimize delays in procuring materials.

(ix) To conduct studies in areas such as quality, consumption and cost of materials so as to minimize cost of production.

(x) To train personnel in the field of materials management in order to increase operational efficiency.

Purchasing or Procurement:

The purchasing department occupies a vital and unique position in the organisation of an industrial concern because purchasing is one of the main functions in the success of a modern manufacturing concern. Mass production industries, since they rely upon a continuous flow of right materials, demand for an efficient purchasing division.

The purchasing function is a liaison agency which operates between the factory organisation and the outside vendors on all matters of procurement. Purchasing implies – procuring materials, supplies, machinery and services needed for production and maintenance of the concern.

Objectives of Purchasing Department:

(i) To procure right material.

(ii) To procure material in right quantities.

(iii) To procure materials of right quality.

(iv) To procure from right and reliable source or vendor.

(v) To procure material economically, i.e., at right or reasonable price.

(vi) To receive and deliver materials at:

a. Right place, and at

b. Right time.

Purchasing department has to perform certain activities, duties and functions in order to achieve the above mentioned objectives.

Activities, Duties and Functions of Purchasing Department:

(i) Keep records-indicating possible materials and their substitutes.

(ii) Maintain records of reliable sources of supply and prices of materials.

(iii) Review material specifications with an idea of simplifying and standardizing them.

(iv) Making contacts with right sources of supply.

(v) Procure and analyze quotations.

(vi) Place and follow up purchase orders.

(vii) Maintain records of all purchases.

(viii) To make sure through inspection that right kind (i.e., quantity, quality, etc.) of material has been purchased.

(ix) To act as liaison between the vendors and different departments of the concern such as production, quality control, finance, maintenance, etc.

(x) To check if the material has been purchased at right time and at economical rates,

(xi) To keep an uninterrupted supply of materials so that production continues with least capital tied in inventories.

(xii) To prepare purchasing budget.

(xiii) To prepare and update list of materials required by different departments of the organisation within a specified span of time.

(xiv) To handle subcontracts at the time of high business activity.

(xv) To ensure that prompt payments are made to the vendors in the interest of good public relations.

Purchase Organisation:

Purchasing department is a staff function in the overall company structure (Refer Fig.23.1).

The internal organisation of the purchasing department is on a line basis, with purchasing agent, director of purchases or purchasing manager being the incharge of purchase department. He is responsible for the overall efficient operation of the department. The purchasing manager is, however, assisted in purchasing by a number of assistants and a few clerical staff (refer Fig. 23.1). The purchasing manager has the powers to execute purchasing contracts for the concern.

He divides the duties among the assistants according to the nature of purchases to be made. For example, one assistant may purchase only electrical goods, another (major) raw material, third plant equipment and so on. This functional division of efforts makes for increased specialisation and gives a chance to the assistant to better feel and know the market, he is assigned. Fig. 23.1 shows an organisation of a typical purchasing department.

There are three main sections namely purchasing, purchase service and records:

1. Purchasing section places orders with the vendors.

2. Purchase service section follows the progress of the order at vendor’s end, its shipment by the vendor and its final receipt in the company.

3. Records section maintains all records of quotations, costs, purchases, etc.

Centralized and Decentralized Purchase Organisations:

1. The problem of centralising or decentralising the purchase activities arises in large organisations-particularly in multi-plant industries.

Advantages of Centralized Purchasing:

The centralization of purchasing:

(i) Almost invariably makes for more efficient ordering of materials;

(ii) Forms a basis to gain bargaining advantage;

(iii) Eliminates duplication of efforts;

(iv) Helps procuring uniform and consistent materials;

(v) Simplifies purchasing procedure;

(vi) Simplifies the payment of invoices; and

(vii) Permits a degree of specialization among buyers.

Disadvantages of Centralized Purchasing:

1. Centralized purchasing is little slower and more cumbersome than decentralized purchasing.

Applications of Centralized purchasing:

1. For concerns using few materials whose quality and availability are vital to the success of the concern.

2. For purchasing small items of fairly high value such as tool bits, grinding wheels, dial gauges, etc., as well as those for which bigger quantity discounts can be obtained.

Advantages of Decentralized Purchasing:

1. Improved efficiency.

2. Faster procurement of materials.

3. Control over purchases is no longer remote.

4. Decentralized operations are more flexible.

Disadvantages of Decentralized Purchasing:

1. Less quantity discounts.

2. Involves duplication of efforts.

Applications of Decentralized Purchasing:

1. Where different plants of a large organisation require quite different types of materials.

2. Where branch plants require heavy and bulky items such as oil products, fuels, paints, etc.

3. Where purchases are to be made within the local community to promote better public relations.

Buying Techniques:

Materials can be bought or purchased by one of the following techniques:

(a) Spot Quotations:

The buyer can go to the market, collect minimum three quotations (for purchasing one material) from different suppliers, take a spot decision, pay cash and buy the commodity.

Generally the item is purchased from the vendor who furnishes a quotation of least price.

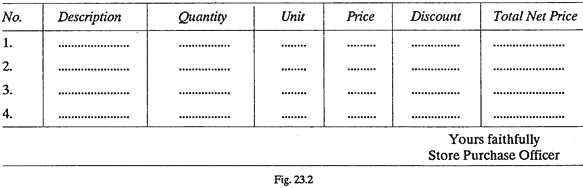

(b) Floating the Limited Enquiry:

A few reliable (and otherwise registered with the company) vendors are written letters to send the price and other details for a particular commodity.

A quotation form as shown in Fig. 23.2 is generally used for calling the quotations:

2. Submit quotations in duplicate.

3. Preferably quote in the same order as in the enquiry letter.

4. Price each item separately and the prices quoted should be for destination……

5. If you are unable to furnish materials as per our descriptions and wish to offer a substitute, please give details.

6. Quotations should be valid for at least one month from the date of opening.

7. Taxes should be mentioned for each case.

8. Quotations should be sent in sealed covers.

9. The right is reserved to accept or reject quotations on each item separately or as a whole.

The quotations will be opened on… at……… in the office of the undersigned.

After getting replies from vendors, the quotations are opened and a comparative statement like one shown in Fig. 23.3 is prepared. The comparative statement helps studying and comparing different quotations at a glance and a quick decision can be taken as with whom to place the order.

Comparative statement is analysed in the light of under-mentioned points and the best quotation is selected for ordering the material:

i. Price of the (article or) material.

ii. Material specifications and quality.

iii. Place of delivery.

iv. Delivery period.

v. Taxes, etc.

vi. Terms of payment.

vii. Validity of tender.

viii. Guarantee period, etc.

(C) Tenders:

A tender or a quotation is in the form of a written letter or a published document (in newspapers). The aim is to find the price for procuring certain materials or to get a particular work done within the desired period and under specified conditions.

Types of:

The tenders may be of the following three types:

1. Single tender.

2. Open tender.

3. Closed tender or limited tender [Please refer to section 23.4(b)].

1. Single Tender:

Tender is invited from one reliable supplier only. Single tender is called under following conditions:

a. Proprietary items.

b. High quality items.

c. ‘C’ class items such as clips, pins, pencils, etc.

d. When items are required comparatively urgently.

2. Open Tender:

Open tender which is also called press tender is published in Newspaper, Trade Journals etc., for procuring materials of desired specifications.

a. It is open to everybody; any vendor (reliable or unreliable) can furnish the quotations.

b. Open tender gets very wide publicity.

c. A vendor has to deposit an earnest money with the tender information. This is just to ensure that the vendor does not back out from the rates etc., which he submits.

d. Given below (Fig. 23.4) is a typical example of tender notice published in Newspaper:

Earnest Money:

Earnest money is demanded from the supplier who quotes the tender so that later on he does not back out from the rates he quotes for supplying the material or goods.

Security Deposit:

After selecting the supplier to whom to give the tender, either on the basis of lowest rates quoted by him or otherwise, he is asked to make a security deposit so that in case the supplier fails to furnish the goods properly and in time, the security deposit can be forfeited.

Quantity and Quality Standards:

Quantity Standards:

There are four important Quantity Standards, namely:

(i) Maximum inventory,

(ii) Minimum inventory,

(iii) Standard order, and

(iv) Reorder point.

These quantity standards have been shown in Fig. 24.1:

Quality Standards:

Quality:

In the purchasing context, QUALITY refers to the suitability of a commodity for its intended use.

Therefore, in purchasing, the best is not necessarily the highest quality; the best quality can be even a lower quality.

Quality Standard:

A quality standard is the description of an acceptable level of quality of a particular item.

Quality standards establish the quality objectives (of a commodity) to be measured or evaluated. In the past three decades, industry has seen a tremendous advance in the preciseness of its quality standards; quality has changed from a generic art to a specific science with definite quality standards and instruments to measure and compare the characteristics of a product against the quality standards set.

The necessary quality standards for a particular product are stated on the drawing in terms of dimensional tolerances or written into the test Specifications. The manufacturing department then makes products as per these standards and the inspection division inspects the products to the same standards.

Drawings show the shape and the exact dimensions and the tolerances permitted on the product whereas Specifications describe such characteristics as colour, chemical composition, mechanical properties (i.e., tensile strength, hardness), kind of raw material etc.

Specifications can be in the form of:

(a) Dimensional and material specifications. They must consist of a list of physical or chemical properties desired in the product. Raw materials, oils and paints are specified this way.

(b) Performance specifications. They indicate the performance or use of the purchased item, for example, a component may be specified as capable of bearing a reverse bend at 100°C temperature.

(c) Blue prints. Blue print is the most precise and probably the most accurate of all types of descriptions and it finds applications where close tolerances or a high degree to mechanical perfection is desired.

Both drawings and specifications describe what the product should be like after it has been made.

Quality standards are dictated by the following requirements:

(i) The efficiency with which the product can perform its function.

(ii) The cost and the estimated life of the product.

(iii) The quality of interchangeability and the ease of making assembly.

(iv) Appearance and FEEL of the production in use.

Accounting:

All purchase transactions initiate a chain of accounting transactions taking from charging the transaction to the proper account to the final payment of the bill. Basically, the checking of invoices is an accounting procedure which can be handled efficiently by the accounting department but unluckily when accounting department does so, it becomes a mere clerical routine procedure.

Checking of invoices involves technical features also such as it’s (i.e., invoice’s) compliance with the description and specifications contained on the purchase order. For this reason and since large company funds and significant discounts are involved in accounting tasks, there should be close coordination between purchasing and accounting departments.

Stores and Material Control:

Materials and supplies constitute the most important assets in the majority of business enterprises. The success of the business, besides other factors, depends to a large extent on the efficient storage and material control.

Material pilferage, deterioration of material and careless handling of stores lead to reduced profits. Even losses can be incurred by concerns in which the store-room is available to all employees without check as to the quantities and purpose for which materials are to be used.

Requirements of a Material Control System:

1. Proper coordination of departments such purchase, receiving, testing, storage, accounting, etc.

2. Making economy in purchase and use of materials.

3. Operating an internal check to verify all transactions involving materials, supplies, equipment, etc.

4. Storing materials and supplies properly in a safe place.

5. Operating a system of perpetual inventory to find at any time the amount and value of each kind of material in stock.

6. Setting of quantity standards.

7. Operating a system to see that right material is available to a department at the time of its need.

8. Keeping proper records of all material transactions.

Stores Management:

Stores management takes care:

1. That the required material is never out of stock;

2. That no material is available in (much) excess than required;

3. To purchase materials on the principle of economic order quantity so that the associated costs can be minimized; and

4. To protect stores against damage, theft, etc.

This can be achieved through:

1. A proper purchasing practice (i.e., when to order materials).

2. An adequate procedure of receipt and issue of materials.

3. Proper methods of storing materials.

4. An effective system of physical control of materials.

5. A proper method of keeping store records.

Functions of Stores Department and the Duties of the Storekeeper:

1. To receive materials, goods and equipment, and to check them for identification.

2. To receive parts and components which have been processed in the factory.

3. To record the receipt of goods.

4. To correct positioning of all materials and supplies in the store.

5. To maintain stocks safely and in good and condition by taking all precautions to ensure that they do not suffer from damage, pilfering or deterioration.

6. To issue items to the users only on the receipt of authorised stores requisitions.

7. To record and update receipts and issues of materials.

8. To check the bin card balances with the physical quantities in the bins.

9. To make sure that stores are kept clean and in good order.

10. To prevent unauthorized persons from entering the stores.

11. To make sure that materials are issued promptly to the users.

12. To plan store for optimum utilisation of the cubic space (i.e., length, breadth and height).

13. To ensure that the required materials are located easily.

14. To initiate purchasing cycle at the appropriate time so that the materials required are never out of stock.

15. To coordinate and cooperate to the full extent with the purchasing, manufacturing, inspection and production planning and control departments.

Location and Layout of Stores:

Location:

1. Location of the stores should be carefully decided and planned so as to ensure maximum efficiency.

2. The best location of stores is one that minimizes total handling costs and other costs related to stores operation and at the same time provides the needed protection for stored items and materials.

3. Store location depends upon the nature and value of the items to be stored and the frequency with which the items are received and issued.

4. In general, stores are located close to the points of use.

Raw materials are stored near the first operation, in-process materials close to the next operation, finished goods near the shipping area and tools and supplies in a location central to the personnel and equipment served.

5. All departments should have easy access to the stores and especially those which require heavy and bulky materials should have stores located nearby.

6. In big industries having many departments, stores department possibly cannot be situated where it is convenient to deliver materials to all departments and at the same time be near the receiving department; thus it becomes often necessary to set up sub-stores conveniently situated to serve different departments.

This leads to the concept of decentralized stores.

7. In decentralized stores system, each section of the industry (e.g., foundry, machine shop, forging, etc.) has separate store attached with it; whereas in centralised stores system, the main store located centrally fulfills the needs for each and every department.

Advantages of centralisation of stores:

(i) Better supervision and control.

(ii) It requires less personnel to manage and thus involves reduced related costs.

(iii) Better layout of stores.

(iv) Inventory checks facilitated.

(v) Optimum (minimum) stores can be maintained.

(vi) Fewer obsolete items.

(vii) Better security arrangements can be made.

Advantages of decentralisation of stores:

(i) Reduced material handling and the associated cost.

(ii) Convenient for every department to draw materials, etc.

(iii) Less risk of loss by fire or theft.

(iv) Less chances of production stoppages owing to easy and prompt availability of material, etc.

An idea about the disadvantages of centralised and decentralised stores can be had from the advantages of decentralised and centralised stores.

Layout:

1. A good stores layout practice is one which usually brings the point or origin, store-room and point of use in adjacent and proper sequence for best flow of material.

2. Stores layout should be planned with the following objectives:

(i) To achieve minimum wastage of space.

(ii) To achieve maximum ease of operating.

3. Before planning the stores layout:

(a) Classify all store items as follows:

(i) By measurement (i.e., size).

(ii) By quantities (i.e. No. and weight) to be stored.

(iii) By frequency of handling.

(iv) By (material) handling arrangements.

(v) By possibility of perishing the items and the susceptibility to damage.

(b) List the available storage space:

(i) Platforms,

(ii) Floor space,

(iii) Racks,

(iv) Shelves,

(v) Bins,

(vi) Trays,

(vii) Drums, and

(viii) Barrels.

(c) Determine the sequence of laying out storage space for locating the materials:

(i) A Unit. It is the smallest space for storage which is given a particular identity.

(ii) A Tier. A Tier consists of a number of units placed vertically.

(iii) A Row. A row consists of a number of units joined together and spread horizontally.

(iv) A section. A section is made up of a group of rows.

(d) Study the size and shape of the space available for laying out the stores.

4. The following factors should be considered while planning the stores layout:

(a) A section adjacent to the store-room should be kept reserved for the receipt of materials and for its inspection before storage.

(b)Store layout should be such that it provides for easy receipt, storage and disbursement of materials, preferably, nearest to the point of use.

(c) Store-room layout should minimise handling and transportation of materials.

(d) An ideal store-room layout makes optimum utilisation of the floor space and height.

(e) Shelves, racks, bins, etc., should be situated in clearly defined lanes, so that items are quickly stored and located for physical counting or issuing.

(f) Main lanes or aisles should usually be between 1.5 and 3 metres wide, depending upon the type of material and the amount of traffic involved. Sub-aisles between racks and bins may be a minimum of 80 cm wide.

(g) Storage spaces should be clearly marked to ensure easy and quick identification.

(h) Storage space should be adequately protected against waste, damage, deterioration and pilferage.

(i) A place for storing a material should be decided depending upon the material characteristics, e.g., fuels and flammable gases will require separate locations, cement, welding electrodes and ferrous parts need a dry place for storing, etc. Portable and salable items should be stored in areas enclosed with wire-mesh partitioning so that all unauthorized persons can be kept outside that area.

(j) Store layout should be such that for its efficient operation it can make use of modern material handling equipment such as fork-lift conveyor’s, etc.

(k) Store layout should be such that the storekeeper is not compelled to put newly arrived material on the top of the old. As a rule, all the old stock should be consumed first before using the new one.

(l) Due space (20 to 25%) should be left in each portion of the store to allow for expansion.

(m) Figs 23.7 (a) and 23.7 (b) show a poor and a good layout of storage space.

Receipt and Issue of Materials:

Receipt of Materials:

All materials from outside sources are received by the Receiving Department. The receiving department unpacks the goods received and checks quantities and conditions (of the goods). There is a packing slip inside each package that tells what it is supposed to be and usually it gives the purchase order number.

A copy of the purchase order (Fig. 23.6) if it exists with the receiving department, can be made use of to check the items received. Otherwise, a Materials Received Report (Fig. 23.8) is prepared by the receiving department and is sent either to the purchase or to the accounting department to get the same checked against the purchase order.

All the items after they have been received and before they are removed from the receiving department are inspected and sample tested to ensure that the purchase order specifications have been met.

Results of the inspection and tests are indicated in special testing report, upon the basis of which Clearance Report or Rejection Notice (Fig. 23.9) is prepared and Sent by the inspection department to:

(a) Purchase department.

(b) Production department, and

(c) Accounting department.

In case of rejection, a part or whole of the consignment may be returned to the vendor, with a request either for a complete cancellation of the order or for replacement.

Issue of Materials:

1. Materials should be issued by the storekeeper to different departments, only upon receipt of a properly authorized withdrawal form-usually called a Material Issue Requisition form (Fig. 23.10).

Material requisition is prepared in duplicate by the foreman or the manager depending upon the nature and amount of materials or goods to be withdrawn from the stores. Both the copies are sent to the storekeeper who issues the materials and records the quantities disbursed. Both the copies are then forwarded to material accounting division for pricing and entry in the stock ledger.

One copy of the material requisition is retained by the stock ledger clerk to be used as the basis for an entry in the Issued section of the stock ledger accounts. The balance section of the stock ledger accounts is then completed to show the new balance figures for quantity, cost, etc. The second copy goes to the foreman of the department who uses it as the basis for a charge to the appropriate production order for which he prepared the material requisition.

Store Records:

Two records are usually kept of materials and other goods received, issued or transferred- namely on BIN (or STOCK) CARDS and in the STORE LEDGER. Bin cards are written and kept in the stores, whereas store ledger is sometimes maintained by stores office or cost department. This minimises the clerical work of the storekeeper and store ledger, i.e. stores accounting records are kept cleaner and accurate by an experienced personnel in the stores office or cost department.

Bin Cards:

In a store room, materials and other items are kept in appropriate bins, drawers or other receptacles; some items are stacked, while others are racked. For each kind of material, a separate record is kept on a BIN CARD or STOCK CARD which shows details of quantities of each type of material received, issued and on hand each day. The storekeeper maintains bin cards up-to-date. Bin card is attached to each bin or shelf.

A bin card is not considered as an accounting record; it simply informs store-keeper of the quantities of each item on hand. Bin cards may be made in duplicate; one card is attached to the bin (containing the material) and the second remains with the storekeeper on his table for ready reference to the quantity of any materials on hand. A bin card is used as a check on the stock ledger accounts in the material accounting division.

Besides the details of the issue and receipt of materials, a bin card may contain the following information as well to increase it utility:

(i) The maximum and minimum quantity of each material to be carried out.

(ii) Normal quantity of each material to be ordered.

(iii) When certain materials or items require placing orders in advance, (e.g., when purchasing from some foreign country) an ordering level (between the maximum and minimum quantity) may be specified on the bin card so that the materials can be ordered and procured in time.

Bin cards are checked periodically by the stores inspectors to see that they are accurately maintained. Discrepancies, if any, are noted.

Fig. 23.11 shows a BIN (or STOCK) CARD.

Stores Ledger:

Store ledger is identical with bin card except that money values are shown. The ledger is usually of the loose-leaf or card type, each account representing an item of material in store. The store ledger accounts may be maintained by a separate material accounting department or in small concerns by the store-keeper himself. Fig. 23.12 shows a stores ledger account.Entries in ordered section are made as a copy of purchase order is received from purchasing department.

After the material has been received and checked, the entries are made in the Received section from the invoice or the receiving department report. Entries are made in the Issued section from material requisitions received from store keepers for materials issued to different departments.

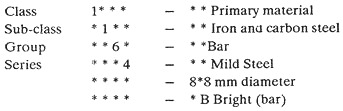

Codification of Materials:

The use of material specification code numbers is an advantage, not only to the purchase department and drawing office, but also to the pricing clerk in the cost department, in that ambiguity is eliminated. Each material or item in the stores should be clearly identified so that the same can be easily located at the time of need.

This is achieved by allocating CODE numbers. The code should be meaningful and impart a unique identity to each material. If a material is described by its trade name, as well as by a serial number and also by its function, it is quite likely that different quantities of the same material might be located at three different places in the same store.

This increases size of the inventory and creates an unnecessary confusion. Codification of materials removes this difficulty and avoids duplication of materials. A code consists of a combination of letters and numbers. The objective is to progress from general to particular.

Examples of material codes:

(a) B.S. 609 means Brass Screw 6 mm x 9 mm

S.S. 815 means Steel Screw 8 mm x 15 mm

(b) Another code may be made up as follows:

Thus 1164-8B implies a bright mild steel bar 8 mm diameter,

(c) ACC/TA/6-implies air-conditioner compressor, top assembly part number 6.

Physical Verification of Stores (Or Stock Taking):

(A) Necessity of:

Physical verification of stores is essential in order to:

(i) Ensure the correctness of stocks held by comparing them with the balance shown in the store ledger or bin cards;

(ii) Avoid shortages of materials in the stock;

(iii) Check losses in inventory due to;

a. Pilferage;

b. Improper storage or misplacement;

c. Deterioration, etc.

(iv) Correct and update store-records;

(v) Calculate the values of stock carried for the balance sheet and profit and loss account;

(vi) Calculate the rate of turn-over of an item;

(vii) Ensure maximum economy in stock carrying;

(viii) Effect insurance covers.

(B) Disadvantages of physical stock taking:

(i) Loss in production; unless and until during period of physical stock taking, plant overhaul etc. is planned.

(ii) Labour and over-time expenses in carrying out stock taking (in order to complete it in a shorter duration of time).

Disadvantages of physical stock taking are minor as compared to the advantages achieved through it.

(C) Methods of physical stock taking:

1. Annual physical verification:

(i) Near the year end, stores are closed for a few days; no material, etc. is issued to any shop in the plant. In case this leads to plant shut down, activities such as repair and overhaul of equipment and machinery are resorted to.

(ii) A team of stores inspectors or stores verifying officers physically check and count each and every item laying in the complete store. They tally it with the quantities marked on bin cards and store ledgers.

(iii) Step (ii) above leads to the formation of a list of surplus and short items. Damaged and obsolete items can also be traced and recorded.

(iv) Inspectors check a number of item everyday as per a preplanned schedule and finish the complete work within a few days.

(v) This method of stock taking is advantageous in the sense that all the items are checked at one time, so there is no confusion about any item being left unchecked.

Moreover, this method helps recording discrepant items at one time and at one place.

2. Perpetual inventory and continuous stock taking system:

(i) Annual Physical verification method may work well for a small plant involving a limited number of store items, because it is not economical to shut down a large plant involving huge inventory quantities for a number of days.

(ii) A more appropriate method for large plants is—the Perpetual Inventory and Continuous Stock Taking System which records store balances after every receipt and issue and facilitates regular checking and obviates closing down of the plant for stock taking.

(iii) Under this system, store items are checked continuously throughout the year; a number of items are counted daily or at frequent intervals and checked (compared) with the bin cards and stores ledger.

(iv) Discrepancies found if any, owing to incorrect entries, breakage, pilferage, over-issue, placing of items in wrong bin, etc., are investigated and corrected accordingly.

(v) Every item of the store is checked atleast once or twice a year.

(vi) To reduce the work load, an item is checked generally when it reaches its minimum level.

Advantages:

The perpetual inventory and continuous stock taking system claims the following advantages:

1. It is not necessary to close down the plant or stop production for stock taking.

2. Since, only a few items are to be checked every day, as compared to annual physical verification, this method is less costly, less tiring, less cumbersome and hence is more accurate.

3. Discrepancies and incipient defects in the stores system are readily discovered and can be rectified before much damage through loss or irregular practices has occurred.

4. Slow moving stocks can be noted and, where necessary, action may be taken to prevent their accumulation.

5. The audit extends to comparing the actual stock with the maximum and minimum level and thus ensures that stocks are kept within the limits specified.

6. Since, stock is kept within the specified limits, the capital invested in the store-items cannot exceed the amount arranged and prescribed for the same.